Is more taxation really the road to prosperity?

Hopefully, govts will focus on broadening tax base by introducing measures to raise more revenues from hitherto undertaxed sectors

Updated Tuesday Jun 03 2025

Updated Tuesday Jun 03 2025

The conventional view in Pakistan’s policy circles is that a higher tax-to-GDP ratio is essential for achieving faster and more sustainable economic growth.

This would certainly support growth if part of the increased revenue is used to reduce the budget deficit, thereby limiting the rise in the public debt-to-GDP ratio and the debt servicing burden. As a result, more fiscal space could be created for growth-promoting spending on key services and critical infrastructure projects.

However, there is a need also to appreciate that imposing more taxes may lead to a fall in the growth rate of the heavily taxed sectors. Therefore, the appropriate strategy is to broaden the tax base and reduce the variation in the incidence of taxes across sectors.

We will look first at the trend in the tax-to-GDP ratio, as well as that of other non-tax revenues over the last decade from 2014-15 to the current year, 2024-25. Projections have been made of the likely fiscal outcome in 2024-25 in the recently released IMF Staff Report, following the successful completion of the first review of the International Monetary Fund (IMF) programme.

The good news is that the total revenues — tax plus non-tax — of the federal and provincial governments combined have increased as a percentage of GDP, from 13.3% in 2014-15 to 15.4% in 2024-25. In particular, the tax-to-GDP ratio has risen from 10.3% to 12.1%.

The first disturbing finding is that the imposition and collection of more tax revenues as a percentage of GDP has not led to any acceleration in the GDP growth rate. The annual average growth rate of the economy from 2014-15 to 2024-25 has been only 3.3%, and it is likely to be even lower in 2024-25 at only 2.6%. This is much lower than the GDP growth rate achieved from 1999-2000 to 2014-15, which was 4.5%.

Why did the additional revenues not yield higher economic growth? The basic explanation is that the revenues were used to finance rapidly increasing current expenditures. The budget deficit increased over the years. Consequently, a rising public debt-to-GDP ratio has implied higher costs of debt servicing. Interest payments have gone up from 4.3% of the GDP in 2014-15 to 7.7% of the GDP in 2024-25.

The ideal outcome of higher tax revenues ought to have been a corresponding jump in development spending. Instead, we see a negative outcome whereby the level of development expenditure of the federal and provincial governments combined has declined sharply from 3.7% of the GDP in 2014-15 to 2.5% of the GDP in 2024-25.

The decline in federal spending on projects in the PSDP has been from 2.1% of the GDP to 0.9% of the GDP.

Consequently, there continues to be substantial underinvestment in critical sectors like water resources, power transmission and distribution, and highways, which are vital for achieving faster growth.

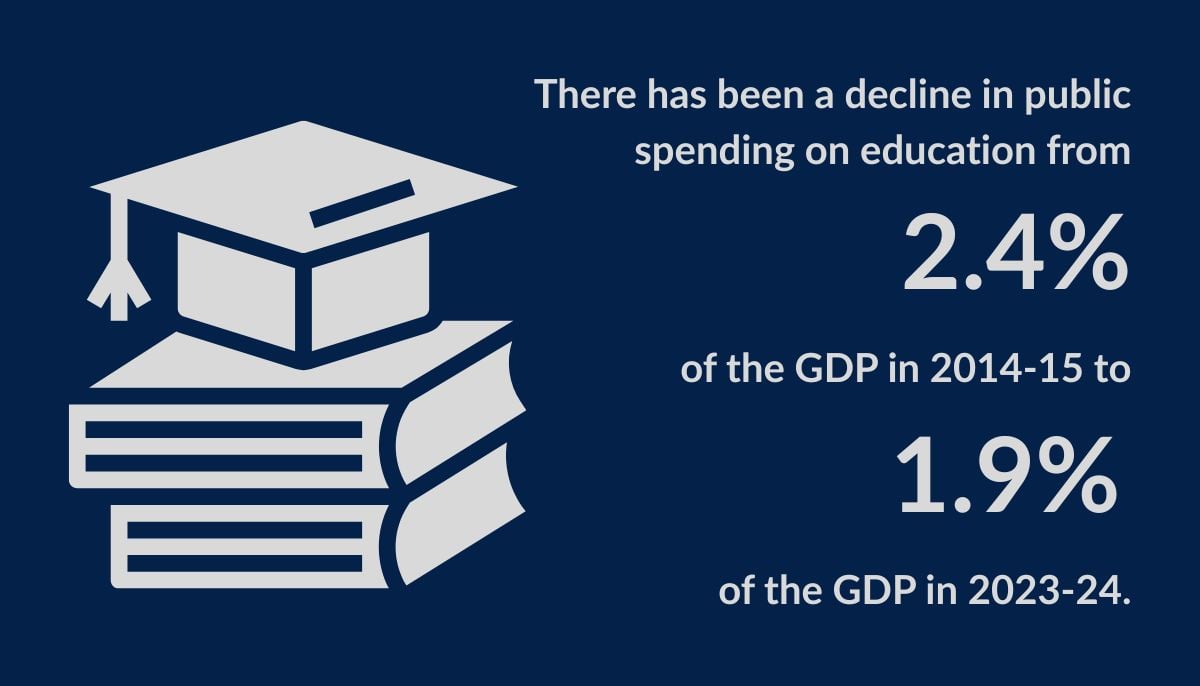

Turning to public outlays on education and health, there has been a negative outcome here also. With the rise in the tax-to-GDP ratio at the federal level and a big increase in the share of the transfers to the provincial governments from the federal divisible pool after the 7th NFC Award, the expectation was that provincial spending on social services would increase substantially. However, there has been a decline in public spending on education from 2.4% of the GDP in 2014-15 to 1.9% of the GDP in 2023-24.

The result is that, over the last decade, the literacy rate has remained more or less stagnant at 60%. The extremely negative development is the big increase in the number of out-of-school children to 26 million in 2023.

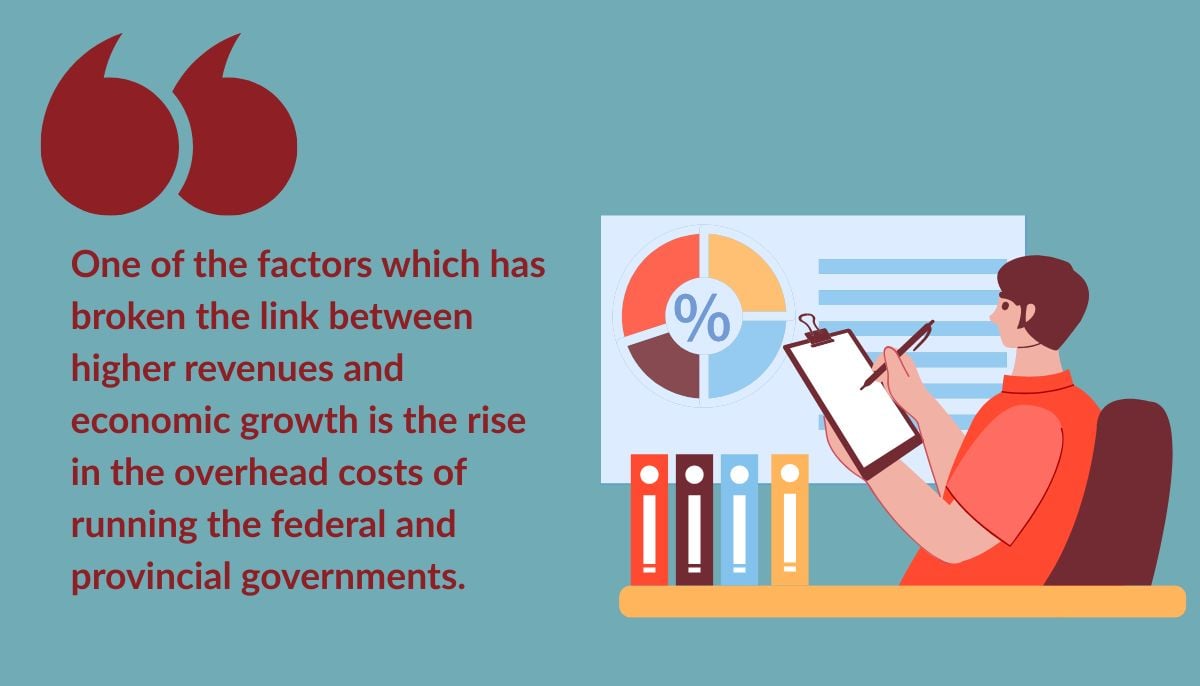

One of the factors which has broken the link between higher revenues and economic growth is the rise in the overhead costs of running the federal and provincial governments. Salaries, allowances, pensions, and operating expenses are rapidly growing and will aggregate to a very high 8.3% of the GDP in 2024-25.

This is due to too many ministries, divisions, autonomous bodies, and attached departments at the federal level, while the provincial governments have substantially expanded their employment.

What, then, should be the appropriate strategy for the mobilisation of tax revenues and their use? The first important measure would be to reduce over-taxation in some sectors of the economy and allow these sectors to breathe and achieve higher growth.

The classic example of a sector that is heavily overtaxed is the large-scale manufacturing sector. It faces a combined direct and indirect tax burden that is four times the burden on the rest of the economy. In effect, almost 32% of the tax revenues are generated from this sector. It is not surprising that the large-scale manufacturing sector has shown a paltry growth rate of only 1.6% since 2014–15. Historically, it has been one of the fastest-growing sectors in the economy.

Other sectors that are relatively overtaxed include mining and quarrying, construction, transport, banking, and insurance. Also, the incidence of personal income tax is five times higher for salaried persons compared to those who are self-employed, with a high proportion in the informal sector.

The very evident strategy is to spread the tax burden to hitherto undertaxed sectors and reduce the incidence in the overtaxed sectors. Fortunately, this strategy has now been adopted under the umbrella of the IMF programme.

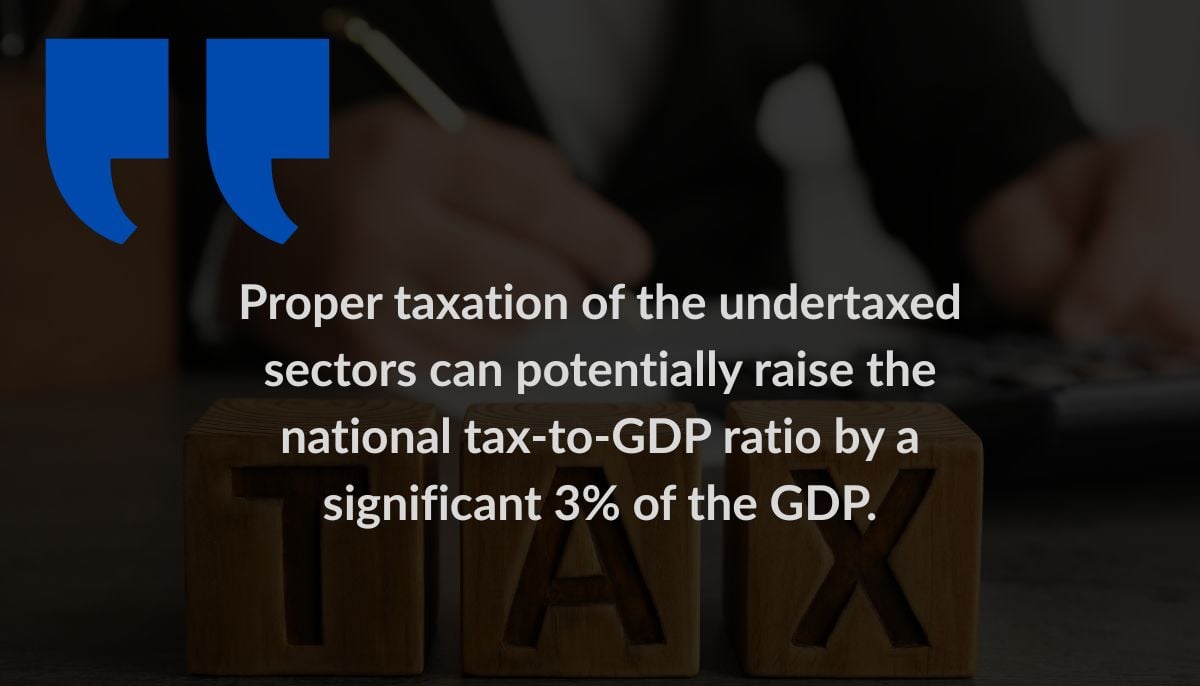

The three grossly undertaxed sectors are agriculture, retail trade, and real estate. Combined, they yield only 0.3% of the GDP today. The income tax revenue potential in the agricultural sector is 0.8% of the GDP. It is augmented by the much skewed distribution of farms: 1% of the farmers own over 22% of the farmland.

The revenue potential from the retail trade sector is 0.6% of the GDP. There are five taxes on property, with a combined yield of only 0.2% of the GDP. This can be quickly enhanced to 1.2% of the GDP. Overall, the broad-basing of the sales tax on services and its integration with the sales tax on goods will yield an extra 0.4% of the GDP. Proper taxation of the undertaxed sectors can potentially raise the national tax-to-GDP ratio by a significant 3% of the GDP.

Simultaneously, the overhead costs of the federal and provincial governments will need to be contained. Debt servicing costs could also be managed through an appropriate interest rate policy and by containing the increase in the public debt-to-GDP ratio. Pensions will have to be linked to monthly contributions from emoluments. The burden placed on the federal budget by the SOEs will need to be reduced through a major programme of privatisation. Overall, these measures could reduce current expenditure by 1.5% of the GDP.

One-third of the increase in tax revenues and reduction in expenditure, combined totalling 4.5% of the GDP, may be used to reduce the budget deficit by 1.5% of the GDP. Similarly, 1% of the GDP may be used to compensate for the reduction of the tax burden on overtaxed sectors, and 2% of the GDP for enhancing outlays on development projects and basic social services.

We await the presentation of the federal and provincial budgets for 2025–26. Hopefully, they will focus on broadening the tax base by introducing measures to raise more revenues from the hitherto undertaxed sectors. Steps will need to be announced for significant containment of current expenditure and its diversion to development spending. A reduction in the tax burden on overtaxed sectors and salaried incomes should also be part of the federal budget. The overall agenda of reforms should eventually pave the way for economic prosperity.

The author is a Professor Emeritus at BNU and a former federal minister.

Header and thumbnail image via Canva