Why Pakistan will not default despite the dismal economic situation

As some economists warn that a default risk is not a hypothetical, the government and a few analysts insist that Pakistan’s economic ship will not sink

Updated Friday Jul 29 2022

Updated Friday Jul 29 2022

Pakistan is among the few countries today in deep financial trouble. The previous PTI-led indebted government spent money it didn’t have to shore up the tottering health system against the coronavirus pandemic, and to provide subsidies on petroleum products. Then the political drama in the wake of a no-confidence motion created unnecessary economic unrest. Moreover, Russia’s war in Ukraine sent wheat and petroleum prices surging and the State Bank of Pakistan (SBP) began raising interest rates to quell inflation.

After the new coalition government was sworn in, it contacted the International Monetary Fund (IMF) — the last ray of hope for the country. While the country reached a staff-level agreement with the Washington-based lender, it is yet to get the final nod from the Fund’s executive board, after which Islamabad will receive a loan tranche of $1.17 billion.

With the delay in the fund’s disbursement, the fate of Pakistan’s economy is hanging in the balance with the local rupee losing over Rs50 against the US dollar in the last three months, and the foreign exchange reserves depleting massively to levels currently below $9 billion. The country currently has an import cover of less than 1.5 months.

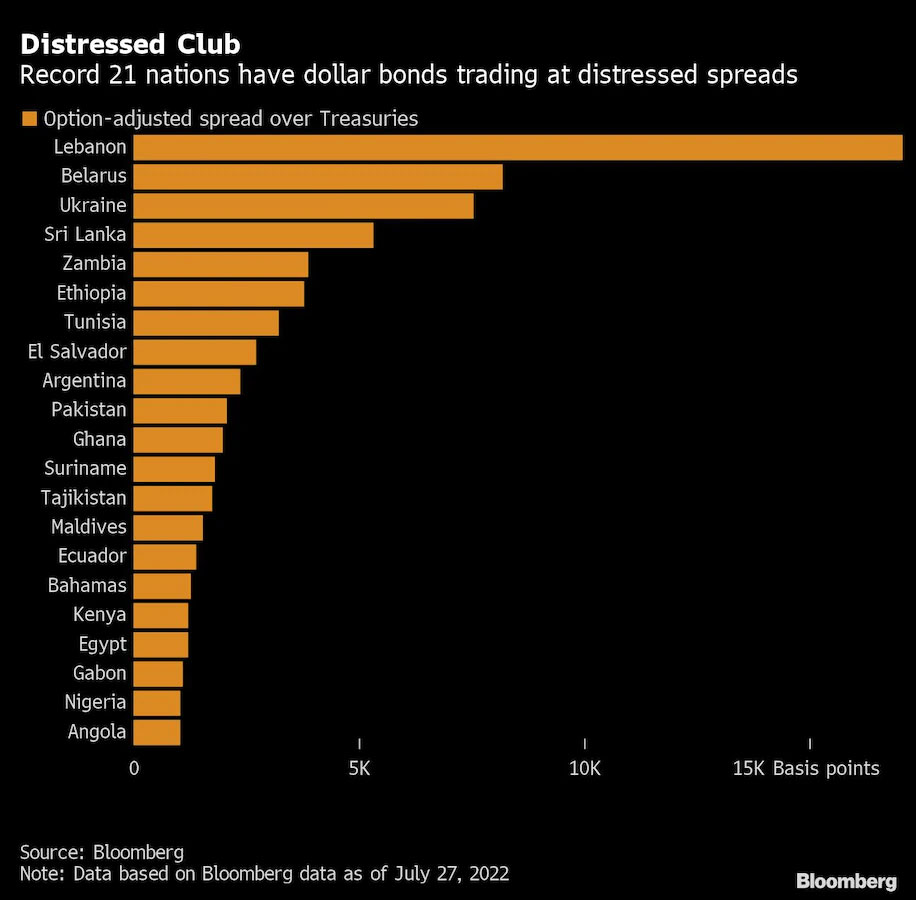

As the US dollar continues to appreciate, the cost of servicing debt can soon become unsustainable because debt is not denominated in the local currency — Pakistan owes in dollars. With this scenario, the question on everybody’s mind is will Pakistan default if the IMF, friendly countries and other donors do not disburse the much-needed billions of dollars?

The coalition government says it is trying to pull the economy out of the quagmire and is trying to maintain a delicate balance between the economic crisis and the political pressure. It is facing the choice of either supporting its struggling population or paying its creditors.

Some financial pundits and economists have sounded the alarm that a default risk and the debt crisis are not hypotheticals; however, the government and some analysts insist that Pakistan’s economic ship will not sink.

Read more: List of countries with highest default risk 2022

Geo.tv reached out to some of the analysts and economists to know the actual risk and whether there are any real chances of Pakistan defaulting.

Let's dive into their takes.

Pakistan has 'enough' foreign reserves

As things stand, Pakistan is unlikely to default on its foreign debt. Pakistan has enough foreign reserves to continue to service its debt obligations. Pakistan's external financing challenge is more strongly tied to the import bill, than the debt servicing obligations.

Much of Pakistan's foreign debt is to other countries and international financial institutions, like the IMF, as opposed to commercial debt which makes managing obligations easier for the government.

A case in point is that much of the debt owed to Saudi Arabia and China are often rolled over easily.

Video explainer: Will Pakistan default?

Pakistan's debt fault lines are two-fold and both are tied to raising new debt, rather than servicing existing ones.

First, can it raise further debt from "friendly countries"? It seems that this time China, Saudi Arabia, and other sovereign lenders are not as forthcoming with new debt as they have been in the past.

Second, can Pakistan navigate difficult global conditions and domestic political crises to raise further private debt, such as through Eurobonds? This seems highly unlikely given the global interest rate climate and the heightened political volatility within Pakistan.

— University of Oxford Economist Shahrukh Wani

‘No imminent signs’

In the current state that we are in, I don't think there are any imminent signs of Pakistan defaulting because the SBP has already confirmed that they have payments that are enough to cover imports and debt servicing for the next fiscal year.

Read more: 'Priority' to save Pakistan from default, says finance minister

Also, Pakistan is in contact with multilateral and bilateral partners, seeking a rollover on the debt repayment as the period for paying them back is getting close.

In light of the Russia-Ukraine war, our lenders are aware that countries such as Pakistan have been unnecessarily hit with high oil prices and inflation, therefore, I am hoping they will take a sympathetic approach.

And then it is to be noted that IMF’s board approval is expected in August, after which World Bank and Asian Development Bank have also assured the Government of Pakistan of assistance — which means their support is linked with the Fund.

Read more: Pakistan's financing needs fully met for this year, assures SBP chief

The pressure on the rupee is essential to address because of the domestic political instability and the government’s decision to not take intrusive measures to control the parity and let the market decide the rates is also a good measure.

So overall, our chances of us defaulting on our import and debt payments are very slim at the moment.

— Sustainable Development Policy Institute Deputy Executive Director Vaqar Ahmed

‘Finance ministry, for now, has arranged over $5bn'

A country defaults when it cannot pay the debt amount after all usual trade and services receipts and payments are met.

It’s all about inflows versus outflows at different points in time. If your outflows are well met with your inflows at various points in time, and you have a good buffer (reserves) in hand for an unforeseen mismatch in these inflows and outflows at any point in time, you are all fine.

Our reserves are low, at 50-60 days of imports, as against global standards of at least three months to a comfortable six months, as well as given the debt repayments coming due within a year.

Read more: Dollar dearth creates dislocation in Pakistan’s foreign exchange market

In Pakistan's context, inflows have now been planned/arranged, but there is more certainty on inflows than on outflows, which leads to a higher risk that turns into greater risk premiums and results in negative market and investor sentiment. Hence, the negative impact on our financial and forex markets, and even more so with increased political uncertainties.

Now, coming to debt repayments that are coming due.

Our bond repayment of $1 billion is due in Dec 2022, and not immediate, while the total gap is around $4 billion, over the course of many months.

By December 2022, the finance ministry, is expected to have arranged over $5 billion (IMF $1.2 billion, friendly countries $3-4 billion cash deposits/rescheduling with oil and gas on deferred payments, sell-off of assets with buyback arrangements), followed by World Bank and Asian Development Bank and other donors with their long-term project and programme funding/debts, offsetting total financing needs for a typical year.

Read more: Fitch, Moody’s expect IMF to disburse funds to Pakistan in third quarter

So, December 2022 has a $1 billion repayment due, which should not be an issue, once the inflows mentioned above are materialised in August-September.

In addition, our current account deficit will be much lower in the coming months (from $2 billion to around/below $1 billion), given the decline in oil and food prices globally, and excessive bans or delays on imports.

All in all, this will slow down the economy; growth in imports, and the supply of US dollars will be much more than what it is now.

Having mentioned all the above, these will all be temporary respites and ad-hoc/stop-gaps, we need structural reforms, stability, and policy consistency with priorities defined, planned, and properly executed.

Otherwise, expect a bigger and unmanageable economic crisis next time.

— Alpha Beta Core CEO Khurram Schehzad

The header and thumbnail image is a representational picture taken from FairObserver