SBP jacks up policy rate to 17% — highest since October 1997

100bps rate hike takes total increase to 750bps since Jan 2022; MPC will now meet on March 16

Published January 23, 2023

- 100bps increase takes total rate hike to 725bps since Jan 2022.

- MPC terms IMF review “critical for reducing uncertainty”.

- Next monetary policy meeting scheduled for March 16.

In line with the market expectations, the State Bank of Pakistan (SBP) on Monday jacked up the benchmark interest rate by 100 basis points to 17% — the highest since October 1997 — to fight the wild inflationary fires spreading across the country.

SBP Governor Jameel Ahmad, in his maiden monetary policy press conference after assuming charge in August, revealed that the committee has observed that “inflationary pressures are persisting and continue to be broad-based”.

“If these remain unchecked, they could feed into higher inflation expectations over a longer than-anticipated period therefore the Monetary Policy Committee (MPC) stressed that it is critical to anchor inflation expectations and achieve the objective of price stability to support sustainable growth in the future,” he further explained.

The central bank raised the benchmark interest rate by 100 basis points (bps) today taking the total increase to 750bps since January 2022 to counter rising inflation.

The MPC — which was constituted as a statutory committee under the State Bank of Pakistan Act — decided to increase the key benchmark rate due to three important economic developments:

- Inflation

- External sector challenges

- Global economic conditions

Explaining each of the aforementioned factors individually, the governor said that despite some moderation in November and December, inflation continues to remain elevated. Importantly, core inflation has been on a rising trend for the past 10 months.

Moreover, near-term challenges for the external sector have increased despite the policy-induced contraction in the current account deficit. "The lack of fresh financial inflows and ongoing debt repayments have led to a continuous drawdown in official reserves," he said.

The MPC also took notice of the global economic and financial conditions broadly remaining uncertain in the near-to-short term, leading to mixed implications for the domestic economy.

The central bank, in its monetary policy statement, further elaborated that the expected slowdown in global demand could negatively impact the outlook of exports and workers’ remittances for emerging economies, including Pakistan.

"This would partly offset the gains from the import contraction. On the flip side, some moderation in international commodity prices may help reduce inflation and the improvement in global financial conditions may also provide some relief to the external sector," he said.

Key MPC observations

- SBP’s baseline GDP growth forecast for FY23 faces several downside risks

- Economic activity as measured through high-frequency demand indicators continues to show moderation

- LSM could potentially show more weakness amid production cuts and supply constraints

- Weaker cotton crop output against earlier expectations could also weaken agriculture sector outlook

- Inconsistency in current fiscal stance with monetary tightening

- External account stress also became visible in decelerated growth in broad money

- Inflation remains elevated due to increase in food inflation

- Core inflation also rose in lieu of higher prices of core goods, especially durables

- Energy inflation remained muted given downward adjustment in fuel prices and reduced fuel costs

- Future direction of fuel costs remain major upside risks to inflation.

- Medium-term inflation target of 5-7% by December 24 unchanged

- Inflation outlook dependent upon anchoring inflation expectations

Current fiscal stance ‘inconsistent’

The committee also noted that the fiscal deficit widened to 1.5% of GDP in the first four months of FY23 from 0.9% in the same period last year, while the primary surplus fell to 0.2% of the GDP, as compared to 0.3% last year.

“The current fiscal stance is inconsistent with monetary tightening,” it mentioned, adding that given the evolving macroeconomic challenges, it is important for the fiscal policy to achieve the planned consolidation in order to help contain inflation and pave the way for sustainable growth.

'IMF review critical for reducing uncertainty'

The statutory committee noted reiterated its November 2022 assessment that the short-term costs of bringing down inflation are lower than the long-term costs of allowing it to become entrenched.

It also emphasised the engagements with the multilateral and bilateral partners to overcome domestic uncertainty and to address the near-term external sector challenges.

In this regard, the MPC viewed the completion of the pending ninth review under the IMF’s External Fund Facility (EFF) as “critical for reducing uncertainty” and unlocking multilateral and bilateral inflows.

‘Anchoring inflation important’

In its forward guidance, the MPC emphasised that anchoring of inflation expectations is important to achieve the medium-term inflation target of 5-7% by December 2024 and “requires coordinated monetary and fiscal policy efforts.”

The statement mentioned that the broad money growth decelerated in the first half (July-December) of the fiscal year 2022-23, “primarily reflecting the stress on the external account”.

On the other hand, domestic credit expanded owing to a seasonal rise in private sector credit along with increased budgetary borrowing because of reduced external financing.

“The disaggregated analysis of private sector credit shows retirement in consumer finance and moderation in working capital and fixed investment loans.”

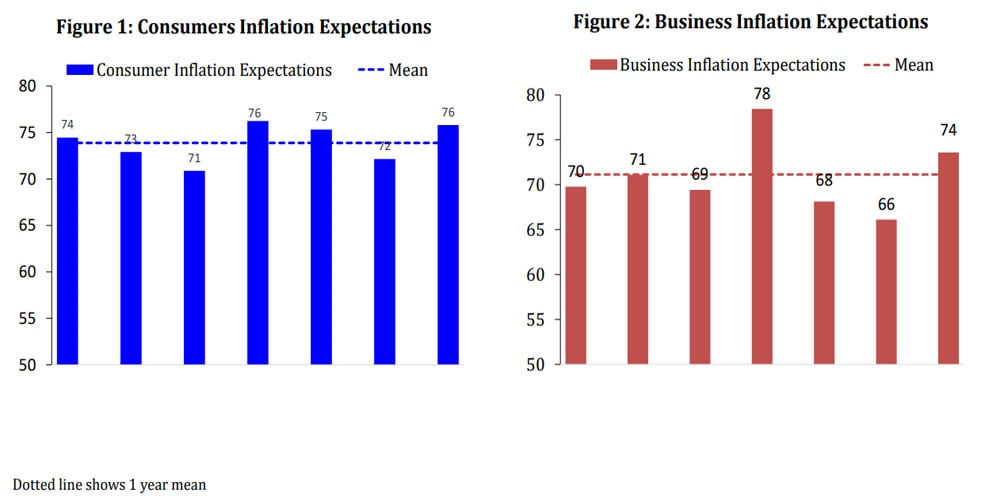

Regarding the inflation outlook, the uncertainty on their future path and expected near-term adjustments remain the major upside risks to the inflation outlook.

“Reflecting these concerns, both the consumer and business inflation expectations have drifted upwards over the short and medium term in latest pulse surveys,” the statement mentioned.