A debt-fuelled budget

Inflation will continue to rise as wage spiral driven by rising salaries and pensions takes hold, purchasing power may be further reduced if inflation rises

Updated Saturday Jun 10 2023

Updated Saturday Jun 10 2023

There are some budgets that are pro-growth, and there are a few budgets that are pro-people, but rarely does one find a budget that is pro-incompetence. The budget for the upcoming fiscal year 2023-24 is not only unimaginative, but further perpetuates the incompetence that plagues the state, and its ability to do something for the people.

The budget outlay increased to Rs14.46 trillion, largely to be funded through additional debt. Almost 50% of the total budget outlay will be used to service debt.

Mark-up payments associated with government debt are expected to cross Rs7.3 trillion, which would make up almost 80% of the tax revenue collected.

The budget will merely increase the already high levels of inflation.

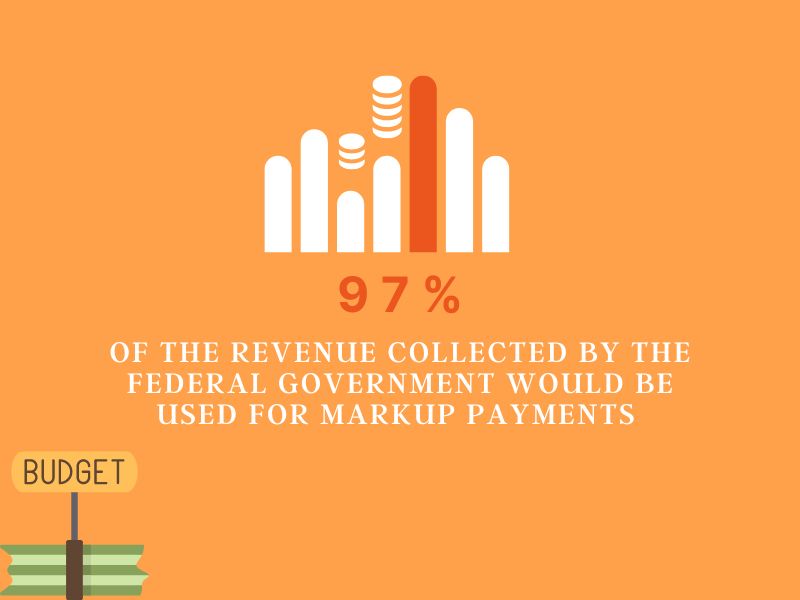

On a net basis, markup payments would make up almost 97% of revenue collected by the federal government. Effectively, whatever tax is being collected by the federal government, almost all of that will go towards servicing mark-up payments.

The formal sector, which is already heavily taxed and has been in financial trouble for many months, is the target of the new taxes. Increased taxes further deter any growth, job creation, or investment, leading to further unemployment in a precarious situation.

Over-taxation would eventually result in prices being passed on to the final consumer, reducing volumes and profitability, and ultimately missing tax collection goals. This will hasten the transition to an unregulated, cash-based economy, which is still thriving.

The tax net was little if at all, expanded by the budget. In an atmosphere where more than a quarter of children under the age of 18 live in poverty, it is creating a climate for increased food inflation instead of widening the tax net.

One characteristic of the state is a failure to learn from past errors. An error that keeps happening is the application of a 0.6% withholding fee on cash withdrawals. The last time a tax of this nature was put into place, it caused a large outflow of capital from the established banking system, which never returned. The amount of money in circulation increased significantly as a result, and it has since continued to rise in order to feed the government's insatiable hunger for borrowing.

Nearly Rs9 trillion worth of currency is now in circulation; if the tax is approved and cash withdrawals begin to occur, the amount of currency in circulation could suddenly increase.

The country's efforts to build tech-based payment systems will be hampered by the tax on cash withdrawals, which will also significantly strengthen the country's shadow economy. As the amount of money in circulation rises, we will witness an increased outflow of deposits from the banking system over the coming weeks or months.

The amount of capital that is accessible in the system will decline as deposits leave the established financial system and the amount of money in circulation rises. the same cash that is utilised to fund the government's borrowing needs and lend to it.

The interest rates at which the government can borrow will rise as the liquidity crisis in the economy worsens because interest rates are merely the cost of money. If there isn't enough money to lend, the cost or interest rate will go up.

Inflation will continue to rise as the wage spiral driven by rising salaries and pensions takes hold.

Although the central bank may play around, there is a significant chance that interest rates will eventually rise further over the next months, partly as a result of unintended consequences of poor policy.

As there is more money in circulation, more people will look for assets on the black market, which will eventually raise prices and feed inflation. The government's debt servicing costs will rise if interest rates rise more, eventually forcing the government to incur more debt to fund its operations.

Inflation will continue to rise as the wage spiral driven by rising salaries and pensions takes hold. The purchasing power may be further reduced if inflation rises.

Numerous industrial units have already been placed inactive due to an inability to secure the necessary foreign currency liquidity, which has also led to a large loss of jobs. There is little chance of real economic development in the absence of a plan to solve the issue, and inflation will keep draining savings and disposable income. Stagflation ruled the previous fiscal year. Failure to address the same will only make matters worse and may even cause hyperinflation.

Because of the government's blatant inability to reduce the fiscal deficit, which is estimated to be Rs7.5 trillion, and the unintended consequences of anti-growth policies, there is a possibility that a perfect storm will develop in which debt will continue to increase quickly, businesses will find it even harder to operate, which will lead to lower tax collections, and eventually a higher than expected fiscal deficit. The fiscal deficit will expand as interest rates rise, eventually requiring more debt to cover it.

The government has continually failed to provide the people with anything. The per capita income will continue to decline as population expansion outpaces anticipated economic development. In spite of the population continuing to grow over the past five years, real earnings have remained constant. It has never been more obvious that the government lacks the motivation and sincerity to implement structural reforms.

The budget will merely increase the already high levels of inflation. While those in charge continue to distance themselves from the actual issues that people are facing, the public will continue to suffer. The government isn't there to serve the people, and it's gotten to the point where there's nothing else it can do but exist.

The writer is an independent macroeconomist. He tweets @rogueonomist

Disclaimer: The viewpoints expressed in this piece are the writer's own and don't necessarily reflect Geo.tv's editorial policy.