Pakistan to repay foreign loans worth $8.638b till June as vulnerabilities multiply

Data shows if Pakistan fails to resume IMF programme by January end, full-fledged crisis will be knocking at its doors

Published January 14, 2022

- If Pakistan fails to resume IMF programme by the end-January, full-fledged crisis will be knocking at its doors, says report.

- In rupee terms, amount for repayment of foreign loans has gone up by 399% during last four years.

- Pakistan's total foreign repayments amount to $12.3 billion during the current fiscal year.

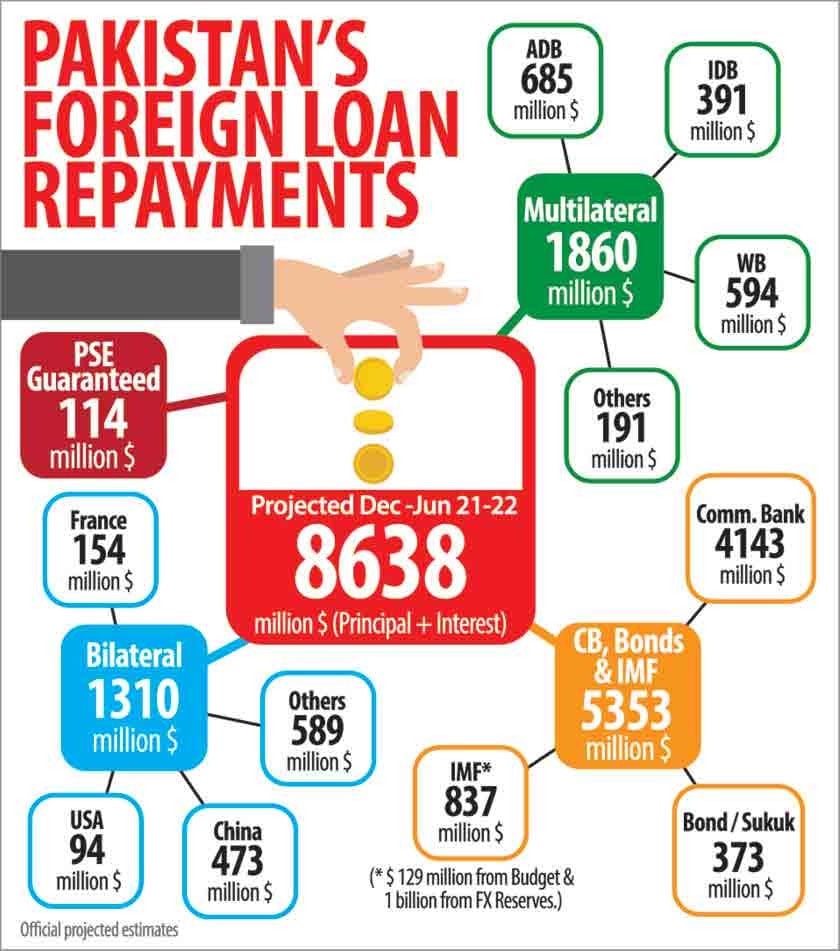

ISLAMABAD: Pakistan has to repay foreign loans worth $8.638 billion during the second half (December-June) of the fiscal year 2021-22, The News reported on Friday, citing official data.

According to the data, in rupee terms that amount for repayment of foreign loans has gone up by 399% during the last four years.

It stood at Rs286.6 billion in 2017-18 and now it is estimated around Rs1,427.5 billion. Meanwhile, in dollar terms, Pakistan had to repay foreign loans — both the principal and mark-up — to the tune of over $12.4 billion.

Keeping in view the ongoing situation of the external sector, if Pakistan fails to resume the International Monetary Fund (IMF) programme by the end of January or early February, then a full-fledged crisis will be knocking at the doors of the country already struggling economy by end of the current fiscal year.

Pakistan’s foreign currency reserves held by the State Bank of Pakistan (SBP) stood at $17.6 billion till December 31, 2021, despite inflows worth $3 billion from Saudi Arabia, over $2 billion from the IMF, $1 billion through International Eurobond in the first half (July-Dec) due to widening current account deficit (CAD).

According to the official data available with The News, the country paid around $3.78 billion on account of principal and mark-up on foreign loans during the first five months (July-Nov) of the ongoing fiscal year.

It is pertinent to mention here that if the IMF programme does not revive till the end of January or early February 2022, then it will become difficult for Pakistan to avoid depletion of foreign currency reserves held by the central bank.

For confirmation, questions were sent to the spokesperson of the Economic Affairs Division (EAD), who confirmed that Pakistan's total foreign repayments amount to $12.3 billion during the current fiscal year, including principal and interest repayments.

'Numbers depict a horrifying picture'

Shedding light on the issue of the increased external sector vulnerabilities, former finance minister Dr Hafiz said: "The situation has become difficult as the country’s external financing requirements climbed to at least $30 billion on a short-term basis."

He further said that the numbers depict a “horrifying picture”. Pasha shared the example of Sri Lanka whereby the country’s foreign exchange reserves stood close to $1 billion but its debt obligations were over $7 to $8 billion.

Pasha elaborated that now Sri Lanka’s foreign minister in his statement, had refused to go to the IMF and indicated that they would approach China to help them to pay off their debt obligations and in return, they might hand over one of their ports to Beijing.

The former minister said that foreign debt obligation has become a “monster” as the country would have to pay back the amount of over $8 billion in the second half of the current fiscal year.

He was of the view that the debt repayment would further escalate in the next fiscal year 2022-23 exactly at a time when the country would be entering into a fever of electioneering after completion of a five-year term by the incumbent ruling regime.

Pasha predicted that the current account deficit might touch $15 to $16 billion for the current fiscal year. In such a scenario, he warned that the foreign currency reserves might start declining, so there are fears of the eruption of a full-fledged balance of payment crisis on the horizon of Pakistan’s economy.

Official data available with The News revealed that Pakistan paid back the principal and mark-up of $3.7 billion on the account of foreign loans during the first five months (July-November) period of the current fiscal year out of which $974 million were paid back to multilateral donors, $34 million to bilateral creditors, $2.74 billion to commercial banks, international bonds, and IMF.

In the second half of the ongoing fiscal year, Pakistan is projected to pay back on account of both principal and mark-up of $8.638 billion out of which $1.860 billion would be paid back to multilateral donors, $1.310 billion to bilateral donors and a major chunk of $5.353 billion to commercial banks, bond/Sukuk and the IMF.

The foreign loan repayment on account of public sector enterprises (PSEs) guarantees is projected at $114 million in the second half of the current fiscal year, so total outstanding foreign debt liabilities climbed to $8.63 billion.

Further research was done by this scribe also revealed that the foreign loan repayments in rupee term escalated manifold in recent years as it stood at Rs286.6 billion in the fiscal year 2017-18 when the PML-N led government ended after the completion of five years.

Currently, foreign loan repayment has been estimated at Rs1,427.5 billion, or 399%. The foreign loan repayment stood at Rs1,228.8 billion in the fiscal year 2020-21, Rs1,095.2 billion in FY20, and Rs601.7 billion in FY19, Rs286 billion in FY18 and Rs443.6 billion in FY17.

The repayment of foreign loans obligations stood at Rs215.9 billion in the fiscal year 2012-13 when the PPP-led government ended its five-year term. The foreign loans repayment stood at Rs132.4 billion during the fiscal year 2009-10.

In a comparison of the last 12 years starting from the fiscal year 2009-10 to 2021-22, the foreign loan repayment escalated from Rs132.4 billion in 2009-10 to Rs1,427.5 billion in 2021-22. It has gone up at supersonic speed, increasing vulnerabilities on the external front manifold.

'Pakistani authorities must remain vigilant'

When contacted, former Director-General Economic Reform Unit (ERU) Ministry of Finance, Dr Khaqan Najeeb, said Pakistani authorities must remain vigilant about country's external financing needs.

These needs can be broadly understood as short, medium- and long-term debt of the country becoming payable during a fiscal year, plus the current account deficit.

The external financing requirement for Pakistan is likely to exceed $27 billion for FY22. This is after assuming that the Chinese safe deposit of $4 billion would be rolled over, he added.

Authorities have to ensure envisaged sources of external funding are more than sufficient to meet these high external financing needs in FY22.

Dr Khaqan highlighted some concerns based on the analyses of the data for the first half of FY22. The debt repayment made on external loans of the government in the first six months is only $3.7 billion.

The annual liability is estimated at $12.4 billion. Therefore, the much higher repayment of $8.7 billion in the second half of FY22 can put pressure on the country’s balance of payments.

He said considering the external needs, Pakistan’s ability to complete IMF's sixth review is thus crucial for securing the $1 billion and for access to other creditors.

The IMF approval can ensure continued access to concessional multilateral financing, private creditors' money, and the country’s ability to float bonds in international markets.

In addition, ensuring a budgeted amount of foreign direct investment is also essential. We must remember all this money is necessary to meet the $27 billion need.

While commenting on the current account deficit explained, he said that it had become larger than initially anticipated. Whereas authorities had initial estimates of 3% of GDP, the current account deficit is likely to now be near 5% of GDP in FY22.

This will be the largest deficit after FY18. The trend of the current account deficit has remained elevated on a monthly basis at an average of over $1.4 billion for the first five months of FY22.

It is hoped the heavy adjustment of the rupee as well other containment measures taken by the authorities are able to bring down the widening deficit in the coming months.

He pointed out three other areas of concern for the balance of payments. In recent months, remittances to Pakistan have begun to decline as the global lockdown is scaled down.

The price of Brent (oil) has bounced back beyond $84 a barrel with some analysts pointing to a rising trend. The rising demand for food and related items continues to hike the import bill like the recent import of urea of 50,000 tons.

The urea shortage in the country could adversely affect the Rabi crops. All these trends could exert pressure on the country’s balance of payment and need sound monitoring by the government and taking timely remedial steps if needed, he concluded.