Buy, hold, or sell Tesla stock in 2026? Expert signal possible weakness ahead

Published January 02, 2026

Tesla (TSLA) faces escalating risks as competition intensifies and delivery momentum softens in the electric vehicle (EV) industry. This raises concerns about whether the EV pioneer remains a buy heading into 2026.

Despite a rebound that more than doubled Tesla’s stock from its 52-week low, analysts state that the recent rally masks deeper structural issues.

The financial reports of the company reveal that the EV registrations fell sharply in Europe, with Germany, France, and several Nordic markets highlighting significant year-on-year declines, even as overall battery-EV sales increased, suggesting Tesla-specific vehicles.

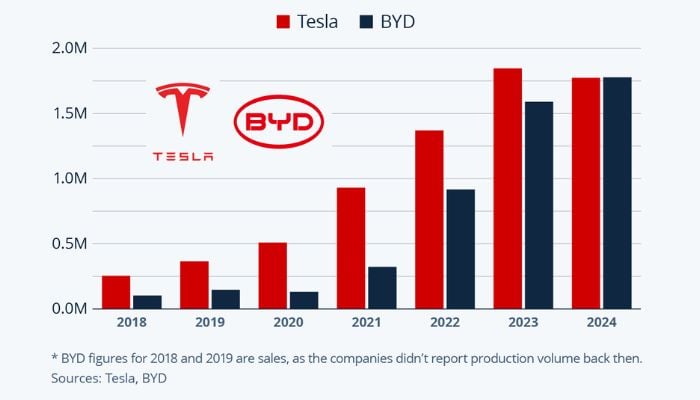

Experts attribute this decline in sales to the growing demand for Chinese EVs. Recent sales data indicate that China’s BYD has dethroned Tesla in EV sales.

Autonomy and robotics are also central to the bearish outlook. Tesla’s ambitious robotaxi rollout faces skepticism, with Alphabet’s Waymo seen as advancing more steadily in driverless services. Similarly, the Optimus humanoid program shows limited progress in production.

Delivery forecast remains cautious. Experts predict that Tesla’s Q4 2025 volumes will fall below 415,000 units, and full-year 2026 volumes may stay under 1.5 million vehicles, well below consensus expectations of 450,000 for Q4. This leaves room for potential downside surprises.

On financial grounds, it is evident that Tesla’s trailing income is declining, while non-cash charges, such as stock-based compensation, are rising. Bearish valuation indicators suggest the stock is overvalued relative to its intrinsic value.

Wall Street analysts give a wide range of one-year price targets, averaging $383.26, suggesting a potential 15% drop from the current price of $449.72.

GuruFocus estimates an even steeper downside of $274.12, implying nearly 40% downside from current levels. Therefore, for investors, Tesla’s path in 2026 may hinge more on execution and competitive pressures than the momentum that fuelled past gains.